bigeman312

Senior Member

- Joined

- Jul 19, 2012

- Messages

- 2,420

- Reaction score

- 2,518

Why not have it be used as a walking path like around Pleasure Bay in Southie?

I fully support a sea wall in Boston and have detailed above how I’d like to see it done.

That being said, it’s important to note that New Bedford’s geography lends itself more readily to a functional seawall. For example, if a seawall were constructed to protect Boston’s inner harbor (from Seaport to Eastie/Logan), it would only be effective to five feet above MHHW. After that, we’d have inundation via the Chelsea Creek from Constitution Beach, Belle Isle Marsh, and Revere Beach.

So, an effective seawall in Boston needs to be a much more involved undertaking than New Bedford, just because of our geography.

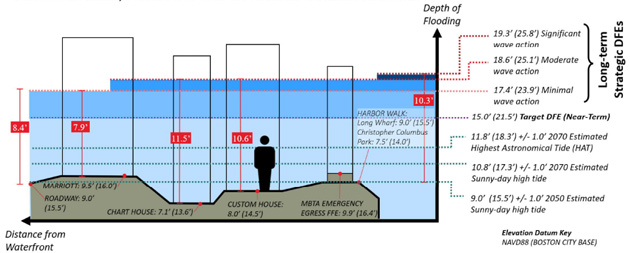

......new resiliency plan, commissioned by the nonprofit Wharf District Council, that outlines $1.2 billion worth of upgrades to the city’s waterfront, from Christopher Columbus Park to the Fort Point Channel and back up to Quincy Market.

The long-awaited plan aims to protect about $3.9 billion in crucial downtown infrastructure, including the Central Artery Tunnel and its entrance, the Harborwalk, tunnels for the MBTA’s Silver and Blue lines and the Aquarium Station, the Rose Fitzgerald Kennedy Greenway, historic buildings, and the city’s electric grid.

Representatives from Wu’s office and the Boston Planning & Development Agency declined to discuss the Wharf District Council plan or its potential impact on the downtown waterfront, e-mailing a statement that said: “The resilience plan is separate from and doesn’t require an update to the Municipal Harbor Plan.”

A likely next step, the city spokesperson said in an e-mail, is to “review this plan through the City’s partnership with the Army Corps of Engineers,” which is studying resiliency efforts across the city — including a potential storm surge barrier underneath a future Northern Avenue Bridge.

New decks and docks would elevate a mile and a half of Boston’s waterfront, protecting downtown from devastating floods. Flood-storage tanks would be built underneath buildings that sit atop pilings, to gather runoff during storms. Sloped shorelines would double as park space — allowing the public continued access even as the city takes steps to protect itself from sea-level rise.

One key player, the New England Aquarium, called the council plan a “pioneering effort” that requires bringing together multiple stakeholders.

“We’ve been really hyper-invested in this,.." [<Rick Musiol, the aquarium’s vice president of external relations ].

...

The collaboration can be a model for other municipalities’ resiliency plans, said Duna Chiofaro, vice president of The Chiofaro Co., the real estate firm behind the proposed tower at the Harbor Garage.

“It’s a necessary step, certainly for this neighborhood, to get on the same page,” he said.

www.bostonglobe.com

www.bostonglobe.com

Chiofaro's plan for the Pinnacle was/is to elevate the base of the building by x feet above Boston City Base. ( I can't remember the exact elevation but recall that one would have up to walk up a flight of steps, or a long ramp to access the ground floor from the Greenway.) The new underground garage would be protected by a moveable barrier. In essence, the Pinnacle would appear like an island as the waters of Boston harbor inundated the surrounding street grid and lapped at the base of other buildings.Also instead of telling chiofaro to gfy wouldnt it make more sense to get concessions from him to help build some of the mitigation measures while redeveloping the site at the same time? Kill 2 birds with one stone. He had already planned on redeveloping the waterfront anyways, they could just make him have to align the development to whatever standard they set for storm mitigation. Makes more sense than paying for it all with taxpayer funds or bonds or whatever. Or are we really going to spend billions on the waterfront and still have the garage at the end? Should be a no brainer.

Another too little too late band-aid.

Fort Point does a Fort Point solution.

Wharf District does a Wharf District solution. It’s all self-interested, shortsighted dike fingering.

We should build a sea wall from Deer Island to Hull to serve the needs of the ENTIRE harbor. And yes we can make it Panamax passable at low tide as extra high tides become the norm.

in less than a decade, Thwaite’s Glacier will break off and throw everyone’s tide estimates into the shredder.

The initial T break off will probably bring king tides 4 or 5 times a year and raise global tides by .6 meters - which doesn’t sound like much, but the lobby of Battery Wharf and every basement on Commercial Street in the North End will flood with 0.3 + king tide + small storm.I agree with the sentiment and would have agreed with every word of this comment as recently as a year ago, but as I’ve learned more about Thwaites, it appears that it’s predicted to have a long duration collapse (watch this comment be jinx and the entire thing collapses overnight leaded to 10 feet of sea level rise globally.)

As far as I understand, based on the current state of scientific understanding, the Intergovernmental Panel on Climate Change (IPCC) estimates a worst-case scenario of up to 1.1 meters (about 3.6 feet) of sea level rise by 2100.

This estimate includes contributions from all sources, not just Thwaites Glacier. If Thwaites were to collapse entirely, it's generally agreed that the process would likely take several centuries to a millennium due to the sheer volume of ice involved.

Rapid action to mitigate and adapt to climate change is still very important.

@BeeLine, perhaps change the thread title to something more general... maybe "Boston Harbor Flood Protection Projects"?

This month, the largest homeowner insurance company in California, State Farm, announced that it would stop selling coverage to homeowners. That’s not just in wildfire zones, but everywhere in the state.

Insurance companies, tired of losing money, are raising rates, restricting coverage or pulling out of some areas altogether — making it more expensive for people to live in their homes.

In Louisiana, the top insurance official says the market is in crisis, and is offering millions of dollars in subsidies to try to draw insurers to the state.

And in much of Florida, homeowners are increasingly struggling to buy storm coverage. Most big insurers have pulled out of the state already, sending homeowners to smaller private companies that are straining to stay in business.

California’s woes resemble a slow-motion version of what Florida experienced after Hurricane Andrew devastated Miami in 1992. The losses bankrupted some insurers and caused most national carriers to pull out of the state.

In response, Florida established a complicated system: a market based on small insurance companies, backed up by Citizens Property Insurance Corporation, a state-mandated company that would provide windstorm coverage for homeowners who couldn’t find private insurance.

For a while, it mostly worked. Then came Hurricane Irma.

The 2017 hurricane, which made landfall in the Florida Keys as a Category 4 storm before moving up the coast, didn’t cause a particularly great amount of damage. But it was the first in a series of storms, culminating in Hurricane Ian last October, that broke the model insurers had relied on: One bad year of claims, followed by a few quiet years to build back their reserves.

Since Irma, almost every year has been bad.

Private insurers began to struggle to pay their claims; some went out of business. Those that survived increased their rates significantly.

https://www.nytimes.com/2023/05/31/...te=1&user_id=da580a4cd1e82ea0128214184976a2acMore people have left the private market for Citizens, which recently became the state’s largest insurance provider, according to Michael Peltier, a spokesman. But Citizens won’t cover homes with a replacement cost of more than $700,000, or $1 million in Miami-Dade County and the Florida Keys.

That leaves those homeowners with no choice but private coverage — and in parts of the state, that coverage is getting harder to find, Mr. Peltier said.

https://www.nytimes.com/2022/10/13/...tion=click&module=RelatedLinks&pgtype=Article“You can’t just build in high-risk areas indefinitely, and expect it to be insurable at an affordable rate,” said Zac J. Taylor, a professor at Delft University of Technology in the Netherlands who focuses on the impact of climate change on insurance and real estate, and who grew up in Florida.

Ian’s aftermath shows how climate change is increasingly eroding the financial underpinnings of modern American life. Without insurance, banks won’t issue a mortgage; without a mortgage, most prospective homeowners can’t buy a home. With fewer buyers, home prices fall, and new development can slow or even come to a stop.

“You need a private insurance market to have a mortgage market,” Dr. Taylor said. “Will working- and middle-class homeownership remain viable in Florida in the long term?”

https://www.nytimes.com/2023/06/04/business/allstate-insurance-california.html?campaign_id=49&emc=edit_ca_20230605&instance_id=94243&nl=california-today®i_id=10059472&segment_id=134711&te=1&user_id=da580a4cd1e82ea0128214184976a2acAllstate, the state’s fourth-largest property and casualty insurance provider, has stopped selling new home, condominium or commercial insurance policies in California, the company said in an emailed statement. It is the latest insurance giant to say it will no longer offer coverage, citing worsening climate and higher building costs that have made it harder to do business in the nation’s most-populous state.

Also this is the extension of the Harborwalk that most Dot residents advocated for as opposed to the current extension being built now that runs behind buildings