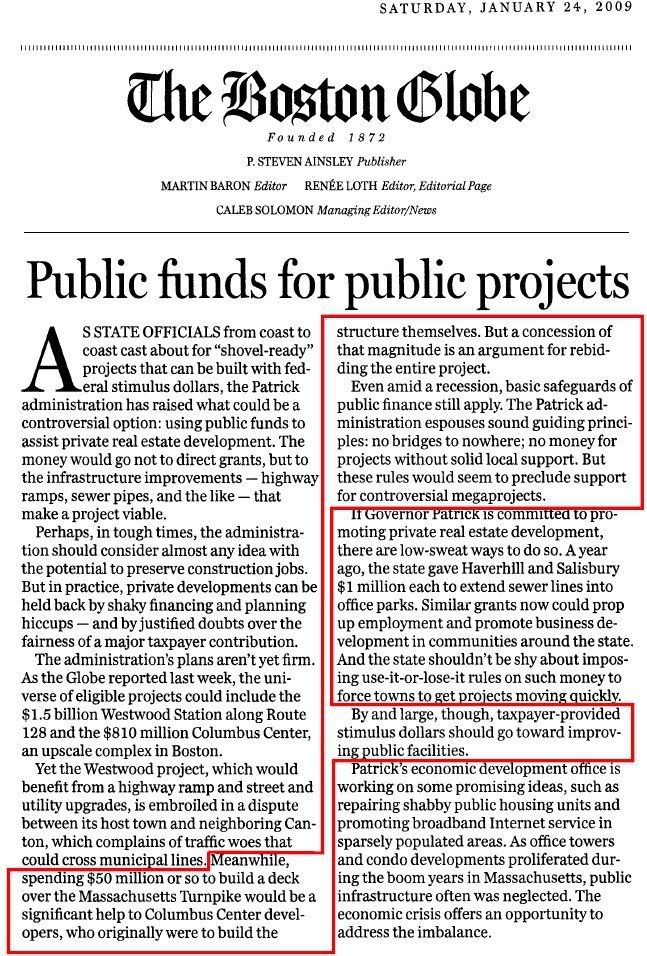

Re: Columbus Center

Hello, Atlrvr.

Since you work for an equity investor, and take limited partnership positions on dozens of deals a year, and have a controlling ownership stake in every deal, you should have no trouble following this sentence-by-sentence response.

_ But if you?re unfamiliar with the Massachusetts forms of TIF and DIF, you?ll need to re-read the local statutes first.

_ And if you?re unfamiliar with the developer?s subsidy applications, you?ll need to re-read those, too.

_

Other Forum members who are not versed ? or interested ? in this topic may recall that public subsidies to Columbus Center?s subsidy-free proposal lie at the heart of the 14-year public controversy.

_ California?s failure to get subsidies to pay their costs and profits also lies at the heart of the fall 2007 decisions by the California-based owners and investors to halt funding altogether.

_ California?s unwillingness to replace the missing subsidies with its own cash is one of the reasons that the proposal has never qualified for any commercial loans.

TIF and DIF financing is paid by future revenues from a project or district.

No, they?re not.

_ Firstly, TIF and DIF financing are different from each other, and Massachusetts TIF and DIF are different from other states.

_ Secondly, there?s no such thing as repayment that is merely ?from a project/district.?

_ Thirdly, all taxes come from a property?s prior owner, current owner, or future owner, and all tax subsidies are paid by taxpayers other than the owner of the subsidized property.

_ Pre-sale taxation during developer construction is not the same as post-sale taxation during condominium owner-occupancy.

_ Finally, taxes lost via a 19-year TIF are never recouped from anyone; the city loses them forever, and taxes lost via a 30-year DIF (which collects full taxes but diverts them to repay a developer?s bond loan) are never recouped from anyone, either; the city loses them forever, too.

_

The calculations are based on additional revenues created, therefore the additional interest and principal liability are covered by the project and adjoining properties (in a DIF).

No.

_ The pre-DIF taxes and the post-DIF taxes are both billed at normal tax rates.

_ Whenever a developer?s bond loan has to be ?covered? (re-paid) by post-DIF tax revenue, the remaining revenue going to the municipality is less than normal, and thus cheats the municipality and all its taxpayers.

_ The full tax revenue gets billed, but the city loses significant portions of everything collected for 30 years, leaving the shortfall to be made up by reduced services and/or tax increases.

It is a net benefit to the city fiscally.

No, it isn?t.

_ Just because a city collects slightly more tax revenue than it used to collect does not mean that the amount collected is a ?net benefit.?

_ Yes, the increased revenue is greater than the former revenue in absolute dollars, but the increased revenue remains far short of what normal tax rates would produce from a given property for 30 years if the normal taxes weren?t being kidnapped to repay a developer loan.

_ For those decades, that shortfall cheats all other taxpayers in the DIF municipality by resulting in reduced services and/or increased taxes.

To say that is costly assumes that it is reallocating tax dollars from other programs or that tax rates must be raised to cover the burden of repaying the issued bonds.

No, it doesn?t assume either reallocation or increased rates.

_ A developer subsidy can be costly even without reallocating dollars from other programs or raising tax rates.

_ Whenever a TIF or DIF collects fewer tax dollars than normal, and those dollars aren?t made up in any other way, and tax rates aren?t raised, that leaves a municipality with fewer tax dollars than called for, which is very expensive in terms of reduced services and permanent opportunity costs.

Since the debt burden is serviced by the increase is revenue of this project, this is fiscally neutral (at a minimal) to the city and state . . .

No, it isn?t.

_ The type of tax revenue used to repay a developer?s debt ? whether pre-subsidy or post-subsidy ? is irrelevant, because whenever any developer debt is repaid from any property tax revenue, the city loses that revenue, and whenever any state income tax is waived, the state loses that revenue.

. . . many projects are fiscally positive since less than 100% of future revenues are allocated to servicing the bonds, therefore the surplus flows to the general municipal tax collections pool.

No.

_ No project can be ?fiscally positive? if it results in any tax revenues being lost, to any source, for any purpose.

_ What you call ?surplus? is not a surplus at all; it is nothing but the leftovers, after subtracting the developer?s bond repayment.

_ Without DIF, all taxes collected go to the municipality; with DIF, only the leftovers do.

The development DOES repay the pricincipal in debt, with the municipality being the "loan servicer".

No, it does not.

_ Look at the Columbus Center DIF to see why.

_ The ?development? exists in two incarnations.

_ When owned and under construction by CalPERS-CUIP-MURC, the development pays no taxes because the property has never paid any taxes, and it still has no value.

_ When owned and occupied by the 1 hotel condominium, the 633 parking space condominiums, and the 443 residential condominiums, the 19-year TIF excuses the development to not pay millions of dollars in taxes, and the 30-year DIF causes the development to remit millions of dollars in other taxes which get kidnapped to repay the developer?s loan instead of going into City coffers.

. . . you are arguing that since my mortgage services escrows my property tax payments and then they are the one to pay the city, that I don't pay property taxes, my mortgage servicer does.

No.

_ No one made that argument.

_ But using your example, you now pay all your property taxes to your mortgage company, and they deliver all your property taxes to your municipality, and all those taxes go into the general fund for police, fire, and schools, just as everyone else?s taxes do, which is as it should be.

_ But if you move into a DIF-sponsored Columbus Center, then you will pay all your property taxes, at full rates, to your mortgage company, and they will deliver those funds to the City, but they get kidnapped to repay the developer?s $130 million bond loan including interest, and those taxes from you will never reach the City treasury.

_ So the DIF cheats the City and all its taxpayers out of the normal tax revenue associated with your property, as it does at all DIF-funded properties.

_ That revenue is permanently lost across 30 years, and is never recouped.

In summary, Massachusetts TIFs and DIFs are gifts to developers that cost the public dearly, each in a different way.

_ TIF subsidies waive millions of the developer?s state income taxes, and millions more in future owners? city property taxes for up to 19 years, whereas DIF subsidies collect full taxes, but divert them away from City coffers to re-pay a developer?s debt for 30 years.

_ TIF waives taxes, and DIF kidnaps them, but both subsidies deprive government of normal tax revenue, starve public services without reducing their workloads, and create pressure for higher tax rates.

A TIF waives taxes and never collects them, and a DIF collects them but uses them to repay a developer?s debt instead of funding the municipality.

_ Either way, government services and all taxpayers are cheated.

This cheating is especially stark at Columbus Center, where the project was proposed as ? and proved by a Certified Public Accountant to be ? subsidy-free and very profitable.

_ No public audit of the costs, revenues, profits, and subsidies has ever shown any need for any subsidy per the Commonwealth?s GAGAS (Generally Accepted Government Accounting Standards).

! And of course, you (nor anyone else) won't move when it happens, because you don't actually believe any of the bullshit you spew, because would you really want you or your kids (if you have one/them) to die 30 years early just to make a political statement on a message board few read? Obviously you'll take your chances, because people have been staying in the Intercontinental, living near the Greenway, and living in much more polluted cities than Boston with no ill health effects whatsoever, and if there were, it would be all over the news! So just pulling out some mythical "UFP" disease out of your ass doesn't actually make it true, because there aren't even any reports of anyone dying or being sickened by them. I'm done pretending to be nice to this noble and principled individual. Besides, you haven't given us full disclosure of your full name, unlike Mr. Keith. Do you want to tell us your middle name? Because we really want to know, and it will be in the best interests of full disclosure that you profess to love. We'd also like to know your job, what vehicles you own, what political contributions you have made, and what money you have received for the Alliance of Boston Neighborhoods. This will not hurt you, only help all of us and you can set an example by telling us your full middle name, which some of us might then follow your principled stand!

! And of course, you (nor anyone else) won't move when it happens, because you don't actually believe any of the bullshit you spew, because would you really want you or your kids (if you have one/them) to die 30 years early just to make a political statement on a message board few read? Obviously you'll take your chances, because people have been staying in the Intercontinental, living near the Greenway, and living in much more polluted cities than Boston with no ill health effects whatsoever, and if there were, it would be all over the news! So just pulling out some mythical "UFP" disease out of your ass doesn't actually make it true, because there aren't even any reports of anyone dying or being sickened by them. I'm done pretending to be nice to this noble and principled individual. Besides, you haven't given us full disclosure of your full name, unlike Mr. Keith. Do you want to tell us your middle name? Because we really want to know, and it will be in the best interests of full disclosure that you profess to love. We'd also like to know your job, what vehicles you own, what political contributions you have made, and what money you have received for the Alliance of Boston Neighborhoods. This will not hurt you, only help all of us and you can set an example by telling us your full middle name, which some of us might then follow your principled stand!