My original statement was coming from common knowledge, based on my personal half a million miles of flying and extensive conversations with other travelers. But in the spirit of a factual debate here's a

USA Today article sourced by an industry professional.

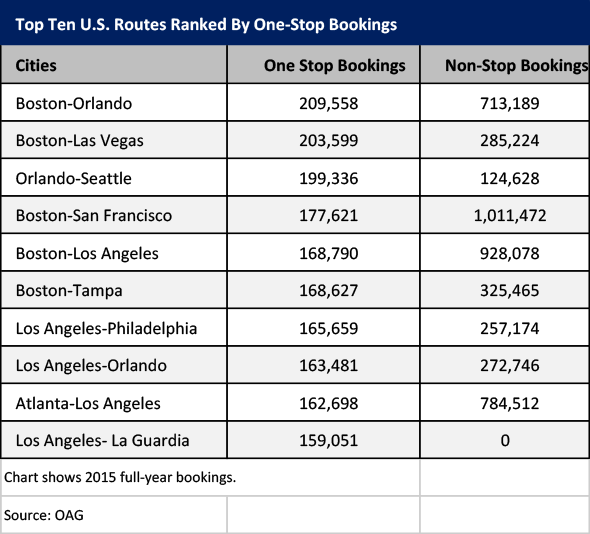

Objectively, non-stop is more convenient than one-stop. I can't see anyone picking a layover instead of a non-stop flight given the same price, unless they wanted to spend some time in the layover city. This means that the demand for non-stop seats is higher. In a perfectly efficient market airlines would match this demand with increased non-stop flights, but unfortunately there are multiple restrictions (slots, pilots, aircraft) stopping them. Instead airlines allocate their resources to the routes with the most business travelers since they can consistently get a higher price from them (ie, business travelers are more price inelastic than leisure travelers). This means that city pairs with a higher percentage of leisure travelers will see a higher percentage of one-stop trips since it's not worth it for the airline to allocate resources to the city pair.